CenterState Signal: The Affordability Challenge Demands a Local Growth Strategy

Posted On |

Image

|

CenterState Signal Q3 2026

The first Federal Open Market Committee (FOMC) meeting under the new Federal Reserve chair made it clear that affordability and prices are the pressure points of the current economy. Following his first meeting as the Fed’s new chair, Kevin Warsh set the tone for possible rate hikes in six words: “The Committee will deliver price stability.” Though the Federal Reserve kept rates unchanged at the June meeting, nine of the 18 participating members (Warsh abstained from submitting) predicted at least one rate hike in 2026.

So, what could a rate hike in 2026 mean for the Syracuse economy?

Rate hikes are intended to slow down price increases, which, as discussed below, the Syracuse metro area is more sensitive to than ever. Prices and affordability are a growing priority for the Syracuse metro region right now – something that historically hasn’t been the major macro concern for the region. We’ve enjoyed the benefits of being a lower-cost metro area, and we want to preserve that as the region experiences historic growth amid rising prices nationwide.

Though rate hikes could ease national price increases, in the short term, a rate hike would increase borrowing costs and could negatively affect housing production at a time when we need to build more than ever.

At a time when we’re more sensitive to national prices and need lower rates to spur development, local policy and financing approaches will be critical to delivering an economy that can grow affordably.

Affordability: Syracuse’s Place in the National Picture

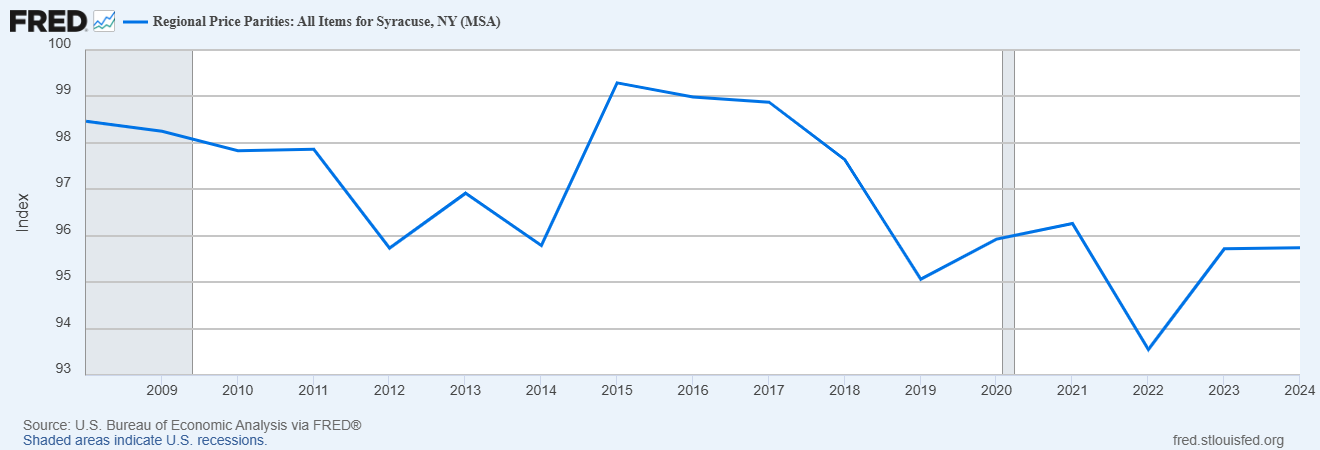

Before examining the impacts rising rates would have on Syracuse, it’s worth considering how the region stacks up nationally. The region is frequently noted as a great place to live or buy a house. Realtor.com ranks cities based on broad criteria such as economic health, amenities and housing availability. But just focusing on regional price parities (RPP1) shows that the Syracuse metro has an affordability advantage over median prices in the U.S.

All items regional prices in the Syracuse MSA are 95.7% compared to the rest of the U.S.:

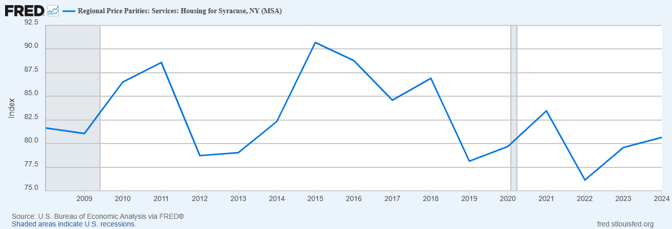

That advantage grows when looking specifically at housing, where prices in Syracuse are 80.7% of the national RPP.:

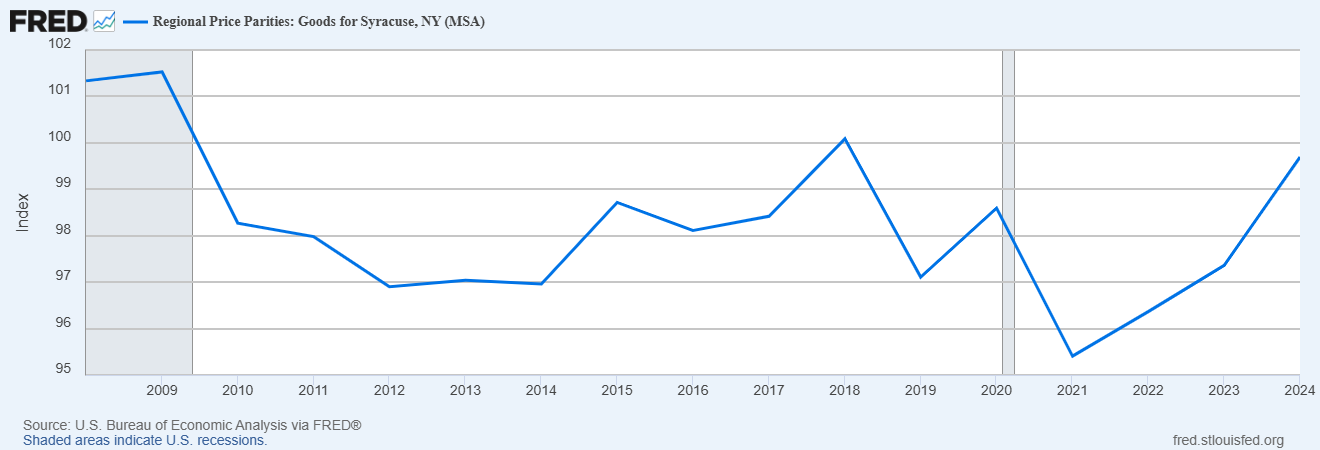

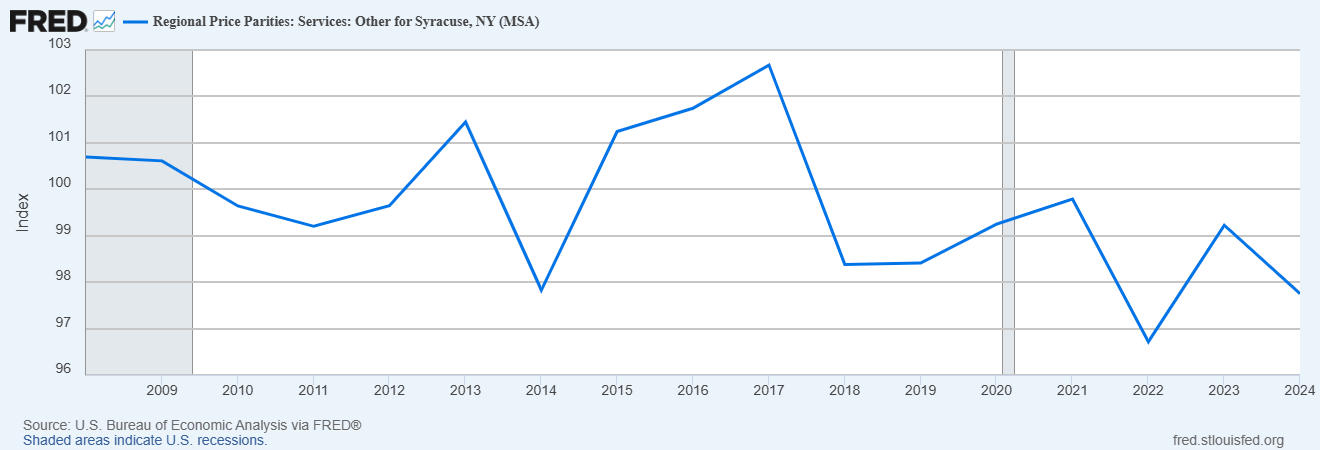

And goods and services are about on par at 99% and 98%:

The RPP data indicate that, in the aggregate, the region has lower median prices than the U.S. as a whole, primarily driven by housing. You could say this is the local “discount” we’re experiencing when we say things are more affordable here, keeping in mind that median statistics are useful for simplifying and clarifying an understanding of data, but they also hide the impacts and experiences of many families and households.

Challenges in Maintaining the Region’s Affordability

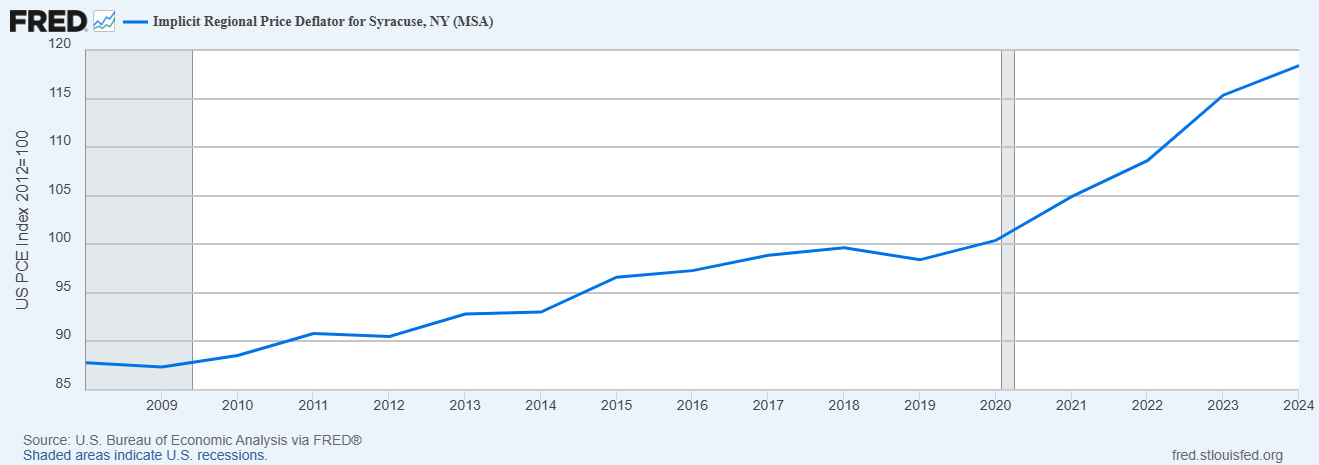

The Syracuse Metro Area still benefits from comparatively favorable average prices, but local inflation is accelerating, something that can be measured with the Implicit Regional Price Deflator (IRPD). IRPD captures both where Syracuse sits relative to the nation and how national prices have changed over time. It's essentially asking: accounting for both local price levels and national inflation, what's the total price change in Syracuse over time? The simplest way to think about IRPD is that it is just a local inflation tracker, and the year-to-year change is the inflation rate.

The slope of the curve is the most useful thing the IRPD tells you. Affordability has clearly weakened as prices have risen from their pre-inflation base. The Syracuse IRPD increased from about 100.4 in 2020 to 118.4 in 2024, meaning the regional price index rose roughly 18% in four years. Assuming that trend continued into 2026, we’ve likely experienced an additional 6-8% inflation.

That does not mean Syracuse has become an expensive metro compared to the national average; other data still shows local prices, especially rents, remain below U.S. averages. It does, however, mean that households and businesses are operating in a meaningfully higher-cost environment than they were just a few years ago. Syracuse’s affordability advantage still exists, but we’ve been dealt a double whammy: an overall reduction in our relative cost advantage amid persistent inflation.

Rising prices are contributing to the growth in households spending more than 30% of their income on rent. From 2019 to 2024, a higher share of renter households were cost-burdened, regardless of income. The share of cost-burdened households earning $35,000 to $50,000 increased from about 30% to 55%; among households earning $50,000 to $75,000 the share more than doubled (9% to 20%).

If the Fed Raises Rates

A Fed rate hike may cool inflation nationally, but in Syracuse’s tight housing market, higher borrowing costs could slow new construction, limit supply and push housing costs higher for renters and buyers.

If a Syracuse apartment project costs more to finance due to rising interest rates, the developer may delay construction, scale back the project, or charge higher rents to make the numbers work. That means a policy intended to cool national prices can have the opposite effect locally: fewer new homes in a market that already needs more supply.

Greater Access to Capital in the Central New York Region

Central New York’s growth strategy benefits from being affordable enough for dynamism in business growth, population attraction and innovation. What’s needed:

- workers to live here,

- employers to hire here,

- developers to build here,

- businesses to expand here, and

- investors to believe the market can absorb growth.

When everyday costs rise, workers need more pay just to stay even. When housing costs rise, recruitment gets harder. When the Fed keeps rates high to fight inflation, capital gets more expensive. That makes housing, construction, business expansion, equipment purchases and real estate investment harder to finance.

The practical solution is to keep doing the work, and to do it with more focus on policies that make it easier and less costly to build:

- Faster and more predictable permit issuance to lower regulation costs.

- More efficient zoning to supply the market and lower development costs.

- Public/private financing structures to make needed projects feasible.

- Develop lower-cost capital to help with interest rates.

- Build more mixed-income and affordable housing for the people who need it.

Central New York already has the right ingredients: a strong affordability position, major state investments in housing and infrastructure, a substantial housing pipeline, and new, unique capital tools like the Housing Central New York Fund.

The task now is to convert that advantage into finished homes at price points the households need. By pairing broad production goals with targeted financing, patient capital, public infrastructure support, and direct tools, we can help build attainable workforce and middle-income housing.

CenterState CEO is tracking roughly $5.5 billion in housing activity across the region. It’s necessary that enough of that pipeline can move through today’s higher-cost environment and still serve the workers, families, employers, and communities driving Central New York’s growth. The region has a clear path: protect affordability by making good projects easier to finance, build and deliver.

1 Regional price parities (RPPs) are price indexes that measure geographic price level differences for one period in time within the United States. For example, if the RPP for Washington, DC, is 120, prices in the District of Columbia are on average 20 percent higher than the U.S. average. An RPP is a weighted average of the price level of goods and services for the average consumer in one geographic region compared to all other regions in the United States. The BEA estimates of real personal consumption and real personal income consist of their respective current-dollar estimates adjusted by the RPPs and converted to constant dollars using the U.S. personal consumption expenditures (PCE) price index.

Other

CEO News